How does buyer cash back work? In plain English, your agent earns a commission on your purchase and gives part of it back to you as a credit at closing. This guide explains how it works in Virginia specifically, where the rules are clear and the savings are real.

In 2026, buyer cash back almost always means a commission rebate or closing-cost credit, not a secret side payment. It has to be disclosed to your lender and structured the right way.

Virginia is one of the states where buyer rebates are legal, and federal regulators treat them as good for consumers. We will get to the rules in a minute.

I am Michael Gorman, Principal Broker at RealtyPeople. 24+ years in Northern Virginia, 2,000+ transactions, $2 billion in volume, Harvard MBA, NVAR Diamond Top Producer. RealtyPeople gives buyers 1% cash back at closing when program rules allow, funded from the commission the seller was already paying.

If you are already shopping in Northern Virginia and want 1% back, start on the Buy a Home page. If you want to understand the mechanics first, keep reading. You can also see how it fits the full buying process.

What does “buyer cash back” really mean in Virginia?

Buyer cash back is a share of the buyer agent’s commission returned to you as a credit at closing. It is not a briefcase of cash after the deal.

Here is the usual structure in Virginia. The listing side offers a commission to the buyer’s broker. The buyer’s broker accepts it. Some brokerages, like ours, share part of that commission back with the buyer at closing.

People use the phrase cash back for three different things. Keep them straight:

- A legitimate buyer commission rebate, credited at closing. This is the model we use.

- Seller concessions, which are closing costs the seller agrees to pay.

- Old cash-back fraud, where the price was inflated and the buyer walked away with real cash. That is illegal and not what this is.

RealtyPeople uses the first one: a commission rebate credited at closing that lowers your cash to close or helps with allowed costs, inside lender and program rules.

Is buyer cash back legal in Virginia?

Yes. Buyer commission rebates are legal in Virginia and recognized as pro-consumer, as long as they are disclosed and lender-approved.

Virginia is one of about 40 states that allow buyer rebates. Only a handful of states still ban them. The U.S. Department of Justice has described commission rebates as a pro-consumer practice that increases competition and lowers costs.

The rules are simple at a high level:

- The rebate comes from the brokerage’s commission, not from thin air.

- It is disclosed in your buyer representation agreement.

- It is disclosed to your lender early and appears on your Closing Disclosure.

One note: this article is general information, not legal or tax advice. Confirm the specifics with your lender, and if needed an attorney or CPA.

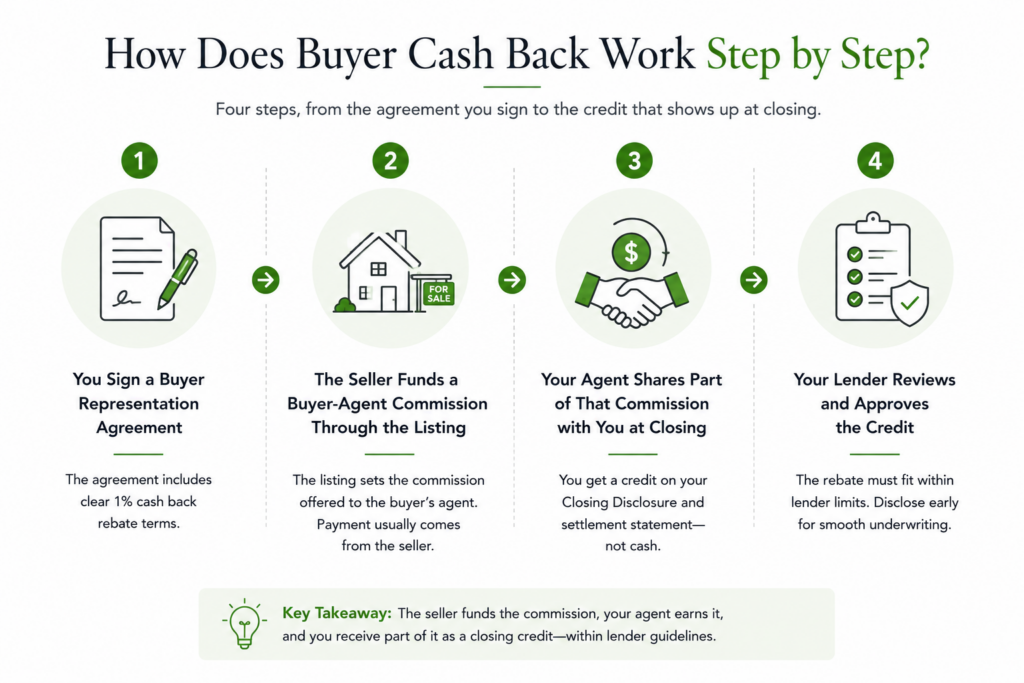

How does buyer cash back work step by step?

Four steps, from the agreement you sign to the credit that shows up at closing. Here is the quick version, then the detail.

Step 1: You sign a buyer representation agreement with clear rebate terms

A buyer-broker agreement spells out how your agent is paid. A good one states exactly how much of the commission is shared with you, when, and how. RealtyPeople writes the 1% buyer cash back into the agreement, so there are no surprises later.

Step 2: The seller funds a buyer-agent commission through the listing

The listing agreement sets any commission offered to the buyer’s agent. After the 2024 NAR settlement, buyer compensation is more often negotiated directly between you and your broker, but the money still usually comes from the seller’s side of the deal.

Step 3: Your agent shares part of that commission with you at closing

Your brokerage instructs the settlement company to apply part of its commission as a credit on your Closing Disclosure and ALTA settlement statement. No suitcase of cash. It is a credit line that reduces your cash to close or covers allowed costs.

Step 4: Your lender reviews and approves the credit

Lenders cap total interested-party contributions and seller concessions, so the rebate has to fit inside those limits. Disclose it early, not at the last minute, so underwriting can clear it without a scramble.

How much can you actually save with buyer cash back?

At typical Virginia prices, even 1% back is thousands of dollars. Caps and program rules decide how much you can actually apply.

Example savings at common price points

| Purchase price | 1% rebate | Example uses |

|---|---|---|

| $400,000 | about $4,000 | most closing costs or a small rate buydown |

| $600,000 | about $6,000 | closing costs plus moving expenses |

| $800,000 | about $8,000 | closing costs, a rate buydown, or upgrades |

Examples only. You can save these amounts when the seller offers a buyer-agent commission of at least 1% and your lender approves the credit. Lenders may limit how much can actually be applied. No outcome is guaranteed.

How buyer cash back interacts with seller concessions and grants

Seller concessions are closing-cost help paid by the seller, capped by loan type: FHA up to 6%, VA up to 4% on certain items, conventional 3% to 9% depending on your down payment.

Virginia Housing also offers a Closing Cost Assistance grant of up to 2% of the purchase price for eligible first-time buyers using a VA or USDA loan, separate from any commission rebate. All credits together, concessions plus grants plus your rebate, must stay within program limits. That is why your lender and agent need to be aligned early.

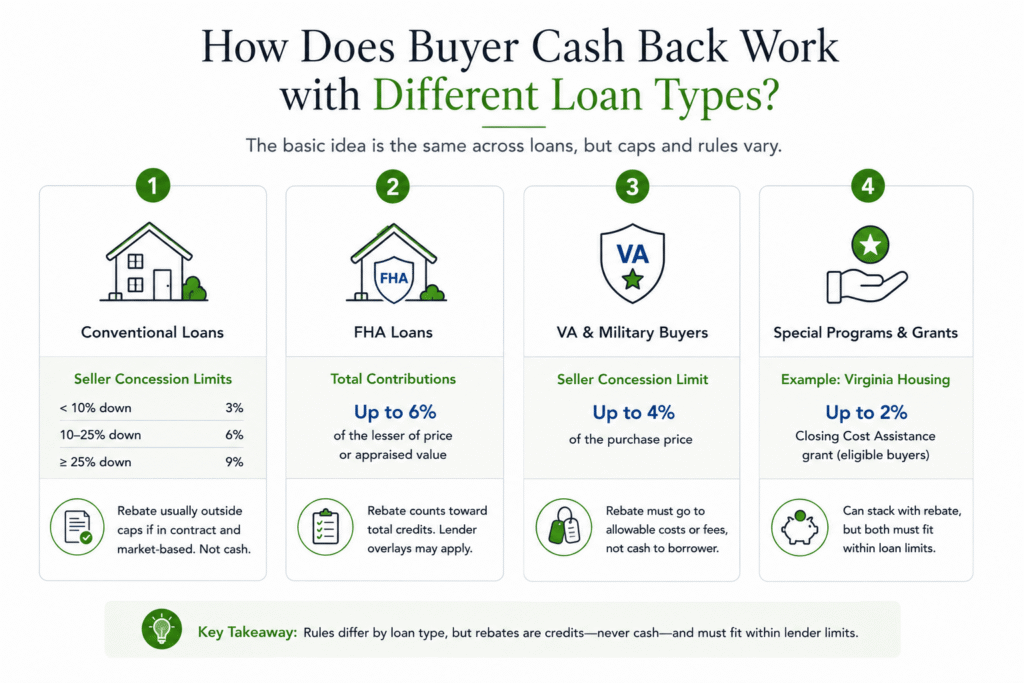

How does buyer cash back work with different loan types?

The basic idea is the same across loans, but FHA, VA, conventional, and special programs each set different caps and rules.

Conventional loans

Seller concessions run from 3% to 9% depending on your down payment: 3% with less than 10% down, 6% with 10% to 25% down, and 9% with 25% or more. Under Fannie Mae and Freddie Mac rules, a commission rebate generally sits outside those concession caps when it tracks market norms and is in the contract, but some lenders still track it as an interested-party contribution. Either way, it cannot come back to you as cash.

FHA loans

FHA allows up to 6% in total interested-party contributions, measured against the lesser of price or appraised value. Your rebate counts toward total credits. Individual lenders may add overlays or extra documentation requirements, so confirm early.

VA and military buyers

VA caps certain seller concessions at 4% of the price and limits actual cash to the borrower. For VA loans, a buyer rebate generally has to be applied to allowable costs or fees, not handed to you as unrestricted cash. VA underwriters watch this closely.

Special programs and grants

State help can stack on top. Virginia Housing’s Closing Cost Assistance grant gives eligible first-time VA and USDA buyers up to 2% of the price toward closing costs, with no repayment. It is separate from a commission rebate, but both still have to fit inside your loan’s overall limits.

How does buyer cash back work with RealtyPeople’s 1% offer?

Our 1% cash back is a commission rebate, credited at closing, paired with full-service representation. Here is how it is built.

Where the 1% comes from

RealtyPeople shares part of the buyer-side commission it receives, equal to 1% of the purchase price, subject to program rules. The seller still covers the buyer-agent commission. The rebate does not add new costs for you.

How it appears on your Virginia closing statement

The 1% shows as a credit on your Closing Disclosure or ALTA statement, applied to closing costs, prepaids, or other allowed charges. There is no off-book payment. Everything runs through the settlement statement, in writing.

What buyers use the 1% for in practice

- Covering some or all of their closing costs.

- Upgrades or post-closing improvements, when allowed.

- Moving costs and furnishing the new place.

Pros and cons of buyer cash back in Virginia

Used transparently and within program rules, the model improves affordability. Used carelessly, it can cause problems.

Advantages for buyers

- Less cash needed at closing.

- More flexibility for repairs, upgrades, and move-in costs.

- A stronger position than buyers with no extra help, especially in a tight market.

Potential downsides and risks

- Lender caps can reduce the portion of the rebate you actually use.

- Revealing the credit late in underwriting can cause delays.

- Treating it as “free money” and stretching your budget, which raises long-term payment pressure.

Red flags to avoid

- Any suggestion of inflating the price to create extra cash back. That can cross into fraud.

- An agent who cannot explain exactly how the rebate appears on your Closing Disclosure.

- No written detail about the rebate in your buyer-broker agreement.

Who benefits most from buyer cash back in Virginia?

It helps several buyer profiles, but the impact is biggest where cash to close is tight.

First-time buyers

1% back can close the gap on closing costs and reduce the need for family help or extra debt. On a $400,000 home, that is about $4,000 toward the costs that catch first-timers by surprise.

Move-up families buying and selling in the same year

Pairing a 1% listing commission on the sale with 1% back on the purchase keeps cash flow manageable across two closings in the same year.

Tech, federal, and military relocators

Rebates lower the stress of a fast relocation and can offset temporary housing or travel, structured as a closing credit. Our Arlington and Alexandria pages cover the submarkets most relocators target.

Investors and second-home buyers

For investors, the rebate can fund repairs or reduce cash outlay. Confirm with your lender and CPA how it interacts with investment-loan rules and tax treatment before you count on it.

How to make buyer cash back work for you without derailing your loan

A simple playbook keeps everything compliant and smooth.

- Talk to a lender early and tell them you plan to use a buyer rebate.

- Confirm how much in credits your loan type allows and how they must be applied.

- Make sure your buyer-broker agreement spells out the rebate clearly.

- Keep your agent, lender, and title company in sync so the credit shows correctly on every disclosure.

- Run your monthly payment with and without the rebate, so you are not over-relying on it.

Quick example: on a $600,000 Northern Virginia purchase, you mention the rebate on your first lender call, the 1% (about $6,000) is planned into your credits, it is written into your buyer agreement, and it shows as a credit on your Closing Disclosure at the table. Clean and on time.

Ready to buy in Northern Virginia with 1% back?

You now know how buyer cash back works in Virginia: legal, lender-reviewed, documented as a credit, and powerful at Virginia price points.

If your next move is in Fairfax, Arlington, Alexandria, Loudoun, or Prince William, start on the Buy a Home page to see how the 1% cash back model works for your price range and loan type.

Frequently asked questions

Exactly how does buyer cash back work in Virginia?

Your buyer’s broker shares part of their commission with you as a credit on the Closing Disclosure. It is legal in Virginia, must be disclosed to your lender, and is usually applied to closing costs or other allowed expenses. It lowers your cash to close rather than paying you cash directly.

Is buyer cash back legal for home purchases in Virginia?

Yes. Virginia allows buyer commission rebates, and federal regulators view them as pro-consumer. The keys are full disclosure in your buyer-broker agreement and lender approval, with the credit shown on your Closing Disclosure.

Can I use buyer cash back for my down payment?

Usually no. Credits can often offset closing costs or prepaids, but most programs do not let them count directly toward the down payment. Check with your lender, since rules and overlays vary by loan type.

Does buyer cash back affect my mortgage approval?

It can if total concessions and credits exceed your loan program’s limits. That is why you disclose the rebate early and let underwriting review the structure. Disclosed correctly and on time, it usually clears without issue.

How much buyer cash back can I realistically get in Virginia?

Some brokerages offer around 1% to 2% of the purchase price, including RealtyPeople’s 1% model. What you can actually use is limited by your loan’s caps on credits and concessions, so confirm the usable amount with your lender.

What is the difference between buyer cash back and seller-paid closing costs?

Both reduce your cash to close, but they come from different sources. Buyer cash back comes from your agent’s commission. Seller-paid costs come from the seller. They are separate line items and often share the same overall program cap.

How do I start the process of buying with 1% cash back in Northern Virginia?

Start on the Buy a Home landing page for a consultation and next steps. We will walk through your price range, loan type, and how the 1% credit fits your purchase.

About Michael Gorman

Michael Gorman is the founder and Principal Broker of RealtyPeople, a full-service brokerage serving Northern Virginia. He holds a Harvard MBA, has 24+ years in the business, 2,000+ transactions closed, and more than $2 billion in volume. He is an NVAR Diamond Top Producer for 10+ consecutive years and a former Senior Vice President at Long & Foster. Mike runs every file personally, start to finish.

View profile →Compliance and disclosures: Savings figures use “can save” examples, not guarantees. A buyer rebate is applied as a credit at closing and is subject to loan-program and lender limits. Commission and concession rules are from 2026 industry and Virginia Housing sources; Northern Virginia price context is from NVAR. No outcome on price, savings, or loan approval is guaranteed. This article is general information, not legal, tax, or lending advice. Confirm specifics with your lender, and an attorney or CPA if needed.

RealtyPeople is a licensed real estate brokerage in Virginia. Michael Gorman is a licensed Principal Broker in Virginia. Equal Housing Opportunity.