Buyer cash back at closing Virginia is a simple idea with one clear rule. It is a legal, lender-approved commission rebate that shows up as a credit on your closing statement, not a side payment of cash handed to you in a parking lot. At RealtyPeople, that rebate is 1% of the purchase price, credited at closing and funded from the commission the seller was already paying.

Here is why it matters. Northern Virginia is one of the most expensive housing markets in the country. NVAR data shows median sale prices in May 2026 near $928,000 in Arlington, $805,000 in Fairfax County, and $770,000 in Alexandria. At those prices, cash to close adds up fast. A credit of 1% can put several thousand dollars back toward your closing costs.

I am Michael Gorman, Principal Broker at RealtyPeople. I have spent 24+ years in Northern Virginia real estate, closed 2,000+ transactions, and handled more than $2 billion in volume. Harvard MBA. NVAR Diamond Top Producer for 10+ consecutive years. I have helped many buyers use a commission rebate to lower their cash to close, the right way, fully disclosed and approved by the lender.

If you already know you want to buy in the next few months, you can start on the Buy a Home page. If you want to understand how the 1% works first, keep reading.

How does 1% cash back at closing work for Northern Virginia buyers?

Your agent earns a commission on the purchase, and RealtyPeople gives 1% of the price back to you as a credit at closing.

Since the 2024 NAR settlement, buyer-agent pay is negotiated directly and is no longer posted on the MLS. But sellers in Northern Virginia still often offer a buyer-agent commission. When they do, we rebate 1% of the price to you at closing.

A commission rebate is not the old, sketchy cash back some people remember. Modern rebates are documented. They appear as a credit on your Closing Disclosure, and they must stay inside lender and loan-program rules.

Here is how RealtyPeople structures the 1%:

- It is sourced from the commission the seller already pays.

- It is applied as a buyer-broker credit on your closing statement.

- It can lower your cash to close, or go toward allowed costs and upgrades, subject to your lender’s guidelines.

| Purchase price | 1% cash back credit | Example use |

|---|---|---|

| $500,000 | about $5,000 | most or all of your closing costs |

| $700,000 | about $7,000 | closing costs plus a small rate buydown |

| $900,000 | about $9,000 | closing costs, a rate buydown, or key upgrades |

Examples only. Assumes the seller offers a buyer-agent commission of at least 1%. The credit is applied at closing and is subject to your lender and loan-program limits. Your numbers can vary.

Is buyer cash back at closing Virginia buyers receive actually legal?

Yes. Buyer commission rebates are legal in Virginia, and federal regulators treat them as good for consumers, as long as they are disclosed and approved by your lender.

Virginia is one of 41 states plus Washington, D.C. that allow buyer rebates. Only a handful of states still ban them.

The U.S. Department of Justice has called commission rebates pro-consumer for years. The DOJ Antitrust Division has worked to lift the remaining state bans because rebates lower prices and increase competition.

Under RESPA, the federal settlement law, a rebate is allowed as long as it is not tied to a referral of business. It has to be shown as a credit on the closing statement, with the party giving the credit named. That is exactly how we do it.

What actually matters:

- Full disclosure in your buyer-broker agreement.

- Your lender’s approval and the concession limits for your loan type.

- Credits usually applied to closing costs, not handed to you as unrestricted cash.

How RealtyPeople handles it: disclosed up front, coordinated with your lender, and shown clearly on the Closing Disclosure. No surprises at the table.

How much can a 1% cash back credit actually save you in Northern Virginia?

At Northern Virginia prices, 1% back often means several thousand dollars less that you need at the closing table.

Sample savings at common Northern Virginia price points

These price bands track Fairfax, Arlington, and Alexandria medians. Use them as a guide, then we run your exact numbers. You can also see local detail on our McLean and Arlington real estate pages.

| Purchase price | Assumption | 1% rebate | What it can cover |

|---|---|---|---|

| $500,000 | Seller offers a buyer-agent commission of at least 1% | about $5,000 | most closing costs |

| $700,000 | Same | about $7,000 | closing costs plus a small rate buydown |

| $900,000 | Same | about $9,000 | closing costs, a buydown, or upgrades |

| $1,100,000 | Same | about $11,000 | closing costs plus a meaningful buydown |

Examples only, not a quote. You can save these amounts when the seller offers a buyer-agent commission of at least 1% and your lender approves the credit. The rebate is applied at closing, within loan-program limits. No outcome is guaranteed.

How buyer cash back compares to seller concessions

Both reduce your cash to close, but they come from different places and follow different rules.

Seller concessions are closing-cost help paid by the seller, capped by loan type. FHA allows up to 6% in total interested-party contributions. VA allows up to 4% of the price on certain items. Conventional loans range from 3% to 9% depending on your down payment. Investment properties are capped at 2%.

A buyer rebate is different. It comes from the buyer-agent commission, not the seller’s concession budget. Under Fannie Mae and Freddie Mac rules, agent-commission payments generally do not count against the 3, 6, or 9 percent concession caps when they track market norms and are written into the contract.

That means a rebate can stack with seller-paid closing costs. The key is to coordinate both early, through your agent and lender, so everything stays inside the rules.

Buyer cash back at closing Virginia: what you need to know

Think of buyer cash back at closing Virginia as a structured, transparent rebate. It is documented, disclosed, and applied as a credit. It is not cash under the table.

- Legal in Virginia. Federal regulators are on the side of rebates, and the practice is well established.

- Lenders care how credits are applied and capped. Underwriters review the credit as part of your file.

- It shows on your Closing Disclosure. That matters for compliance and your tax records. Keep your settlement statement after closing.

- Typical limits apply. Under many loan programs the credit cannot exceed your actual closing costs, and VA loans have their own rules on cash back and reimbursable fees.

Mike’s perspective: In 24+ years, I have seen rebates used well and used badly. Used well, the credit lowers your cash to close and everyone signs off: lender, underwriter, and title. Used badly, someone tries to inflate the price or move money off the books. That is where deals blow up. We keep it clean and documented from day one.

How does 1% cash back interact with different loan types?

The idea is the same across loans, but the caps and mechanics change by program. Know the basics before you shop.

Conventional loans

Seller concessions on conventional loans are tiered by down payment: up to 3% with less than 10% down, up to 6% with 10% to 25% down, and up to 9% with 25% or more down. Investment property is capped at 2%.

Most conventional lenders treat the 1% buyer rebate as a closing-cost credit, not extra cash in hand. Interested-party contributions cannot go toward your down payment, and you cannot walk away with the excess as cash.

FHA loans

FHA allows up to 6% in combined seller and interested-party contributions, measured against the lesser of the purchase price or the appraised value. A buyer rebate has to fit inside that total. Many lenders also add their own overlays on how a rebate is applied and disclosed, so confirm early.

VA loans and military buyers in Northern Virginia

VA caps certain seller concessions at 4% of the price, with strict limits on actual cash to the borrower. For a VA buyer, a commission rebate usually shows as credits toward allowed costs, not pocket cash, and VA underwriters watch this closely.

Many of my clients are PCS movers and Pentagon-area buyers using a VA loan. I coordinate the rebate with the lender up front so it clears VA review without slowing down a tight relocation timeline.

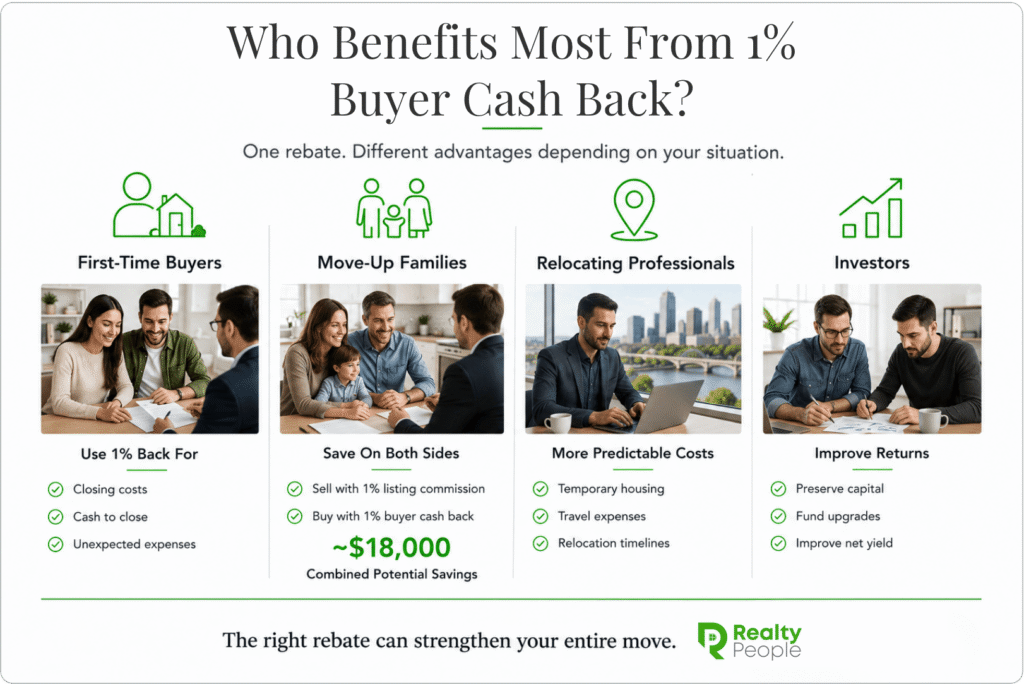

Who is 1% buyer cash back best for in Northern Virginia?

The credit helps several kinds of buyers in different ways, from easing cash to close for first-timers to improving returns for investors.

First-time professional buyers

For a first-time buyer, 1% back can plug gaps in cash to close, cover some or all of your closing costs, or offset a surprise expense. When the rebate is structured right, it does not cost you anything extra out of pocket. You also get the numbers explained in plain English before you write an offer.

Move-up families buying and selling in the same year

You win on both sides. Sell with our 1% listing commission and buy with 1% cash back. On a $700,000 sale plus an $800,000 purchase, you can save roughly $18,000 across both deals. That assumes a 2.5% seller-paid listing commission under a traditional model, separate from any buyer-agent compensation.

This segment carries real stress: two mortgages at once, school-boundary timing, and concurrent closings. I coordinate both closings personally so the timing lines up and the savings show on both settlement statements.

Tech relocators and federal/military relocators

Remote searches and tight relocation windows make predictable costs valuable. A 1% credit can offset temporary housing or travel, applied at closing. For Amazon HQ2 and Pentagon-area buyers, that is real money, and our Arlington and Alexandria pages cover those submarkets in detail.

Investors and second-home buyers

For investors, a 1% rebate can improve net yield or free up capital for repairs and upgrades. One caution: make sure the structure fits your investment-property loan rules and debt-service metrics. Run the numbers with your CPA or lender before you lean on it.

How RealtyPeople’s 1% cash back is different from other Virginia buyer rebate offers

Same core idea as other Virginia rebates, but with a strict full-service model, transparent math, and direct access to a principal broker.

Full-service representation, not a discount call center

Many high-rebate shops hand you a bigger number and far less help. Flat-fee and do-it-yourself models leave you doing most of the work. With RealtyPeople you get the principal broker on every file: 24+ years, 2,000+ deals, from Harvard to housing. Same expert representation, more of your money in your pocket.

One clean offer that aligns with how you already pay

Our model is simple: $500 + 1% for sellers and 1% back for buyers. The rebate uses money already in the transaction. It does not add new charges for buyers. The math is easy to follow, which is the point.

Transparency, lender coordination, and documentation

Your rebate is documented in three places: your buyer representation agreement, your lender file, and your Closing Disclosure. That paper trail keeps appraisers, underwriters, and regulators comfortable. It also protects you, because the credit is in writing from the start.

Step-by-step: how to buy a home in Northern Virginia with 1% cash back at closing

Here is the process from first call to closing, and exactly when the 1% gets locked in.

Step 1: Discovery call and buyer strategy session

On the first call, I explain the buyer representation agreement, how compensation works, and the 1% rebate terms. I ask about your timing, target neighborhoods, loan type, and budget, so the plan fits your real situation.

Step 2: Pre-approval, lender alignment, and rebate confirmation

We loop in your lender early so the rebate is planned from day one, including the disclosure language and the credit caps for your loan. We flag special notes for VA, FHA, and jumbo buyers before you start writing offers.

Step 3: Home search, offers, and negotiation

The rebate is separate from price negotiation, but it is part of your overall affordability. I balance seller-paid closing-cost credits and your buyer rebate so they stay inside program limits. If you want a primer on offer strategy, our post on how much negotiating room a buyer has is a good place to start.

Step 4: Underwriting, appraisal, and final disclosures

The credit appears on your Loan Estimate and again on your Closing Disclosure. Check that the 1% is present and correct. During underwriting and appraisal, the lender reviews concessions and credits, which is one more reason to disclose early.

Step 5: Closing day and what happens to your 1% rebate

On closing day, you usually see the 1% as reduced cash to close, or applied to allowed costs, not a briefcase of cash. Keep every closing document and settlement statement for your records and your taxes.

Common pitfalls and myths about buyer cash back in Virginia

A few myths trip buyers up. Here is the truth, and how to avoid mistakes that can derail a purchase.

- Myth: I can get unlimited cash back at closing. Reality: lender and program caps apply, and under most rules the credit cannot exceed your actual closing costs.

- Myth: Rebates are shady or always illegal. Reality: they are legal in Virginia when disclosed, and the DOJ treats them as pro-consumer.

- Pitfall: off-book cash-back schemes that overstate the price. That invites fraud risk and can void your loan.

- Pitfall: disclosing the rebate late in underwriting. That triggers delays right when you can least afford them.

How I avoid these: disclose on day one, coordinate with the lender, and document everything on the Closing Disclosure. Clean files close on time.

How this pillar fits into your bigger financial picture

The 1% rebate is one piece of a bigger stack: your rate, your term, your price, and your timeline.

Think in terms of total cost of ownership: your payment, maintenance, taxes, and the opportunity cost of your cash. Sometimes the 1% is best used toward closing costs. Sometimes it is better as a rate buydown. That is a conversation for you, me, and your lender together.

A simple comparison on a $700,000 home:

- Scenario A: rebate to closing costs. About $7,000 lowers your cash to close. You bring less to the table on day one.

- Scenario B: rebate to a rate buydown. About $7,000 toward buying down the rate. With 30-year fixed rates near 6.4% in early 2026, per Freddie Mac, a buydown can lower your monthly payment for the life of the loan.

The tradeoff is straightforward. Scenario A helps your cash today. Scenario B helps your monthly payment over time. The right answer depends on how long you plan to stay and how tight your cash is.

Ready to buy a home in Northern Virginia with 1% cash back at closing?

Here is the recap, and the one next step.

- 1% cash back at closing, as a transparent credit on your Closing Disclosure.

- Full-service representation from a principal broker, start to finish.

- Northern Virginia focus in your exact submarkets, from Arlington to McLean to Alexandria.

If you are serious about buying in the next 3 to 9 months, start with a free consultation on the Buy a Home page. We will walk through your numbers, your loan type, and how the 1% credit fits your purchase.

Frequently asked questions

How does 1% buyer cash back at closing work in Northern Virginia?

It is a commission rebate. Your agent earns a commission on the purchase, and RealtyPeople credits 1% of the price back to you at closing. It is funded from the commission the seller already pays, applied to allowed costs on your Closing Disclosure, and disclosed to your lender.

Is buyer cash back at closing Virginia buyers receive legal?

Yes. Buyer cash back at closing Virginia buyers receive is legal when it is disclosed and lender-approved. Virginia is one of 41 states plus Washington, D.C. that allow rebates, and the U.S. Department of Justice treats them as pro-consumer.

Can I use 1% cash back at closing for my down payment?

Usually no. Under most loan programs, credits go toward closing costs and prepaids or a rate buydown, not the down payment. Lender overlays vary, so confirm with your loan officer early.

How does buyer cash back affect my loan approval?

It must stay within concession and credit limits and be disclosed up front. Underwriters review the credit as part of your overall financing package. Disclosed early and documented correctly, it should not be a problem.

Is 1% buyer cash back better than asking the seller to pay closing costs?

They can work together. A buyer rebate comes from the agent commission, while seller concessions come from the seller, so both can reduce your cash to close. Keep total credits within your loan program caps.

Does RealtyPeople reduce service to offer 1% cash back?

No. You get full-service representation from a principal broker with 24+ years and 2,000+ transactions. The savings come from an efficient, higher-volume model, not from cutting service.

When should I talk to my lender about buyer cash back?

As early as possible, ideally before you start shopping. Planning the credit from day one lets your agent and lender structure the deal correctly and avoid last-minute delays.

About Michael Gorman

Michael Gorman is the founder and Principal Broker of RealtyPeople, a full-service brokerage serving Northern Virginia. He holds a Harvard MBA, has 24+ years in the business, 2,000+ transactions closed, and more than $2 billion in volume. He is an NVAR Diamond Top Producer for 10+ consecutive years and a former Senior Vice President at Long & Foster. Mike runs every file personally, start to finish.

View profile →Compliance and disclosures: Savings and cash-back figures in this article use “can save” examples, not guarantees. They assume a 2.5% seller-paid listing commission under a traditional model, separate from any buyer-agent compensation, and they assume the seller offers a buyer-agent commission of at least 1%. Actual amounts depend on your specific transaction, loan program, and lender approval. A buyer rebate is applied as a credit at closing and is subject to loan-program limits. This article is general information, not legal, tax, or lending advice. Talk to your lender and a tax professional about your situation.

RealtyPeople is a licensed real estate brokerage in Virginia. Michael Gorman is a licensed Principal Broker in Virginia. Equal Housing Opportunity.